Capital is money you use to finance the purchase of equipment, supplies and products. Working capital is money you use to cover the day-to-day operating costs of your business. You must consider both when determining your business’s fiscal needs.

For any small business, potential capital outlays can include:

- buildings and facilities

- major equipment

- office equipment and furnishings

- materials, supplies and parts

- initial inventory

When planning capital needs for a start-up, simply calculate the costs of setting up the business. To determine capital needs for an existing business, calculate the costs of growth and expansion, but don’t include items like salaries, utility costs, insurance, and other fixed business expenses.

To determine working capital needs, create projections for accounts receivable, inventory and accounts payable. Compare current, actual costs to your projections. Then subtract the increase in current liabilities from the increase in current assets. The difference is your working capital needs — the amount you will need to keep the doors open.

If you’re seeking capital for a start-up, calculations are easy. You don’t have current actual costs, so the difference in liabilities and assets equals your working capital needs.

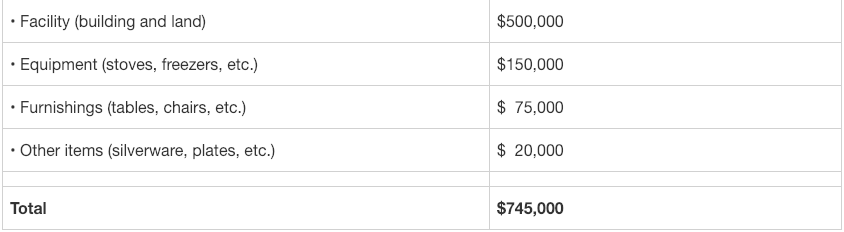

Say you plan to open a restaurant and you estimate the following capital costs:

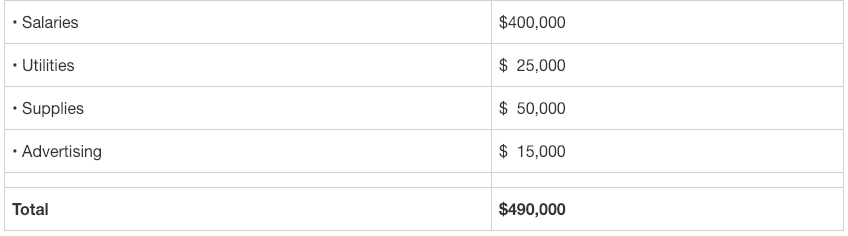

You determine you need $745,000 to open your bistro. But you also need working capital to keep the operation going while the restaurant gains popularity. So, next estimate working capital needs for the first 12 months of business:

The sum of your capital and working capital requirements, $1,235,000, is what you will need to cover the first year of business expenses.

On the other hand, your successful restaurant will generate cash, so develop best and worst-case scenarios.

Let’s say best case you expected to generate $800,000 in sales in that first year. The math is simple: $1,235,000 minus $800,000 equals $435,000. You need $435,000 in capital to open the restaurant under the best circumstances.

Something else to consider: Your projected $800,000 in sales won’t be spread evenly across 12 months. The first few months are likely to be lean until customers discover your restaurant.

To prepare for the unexpected, you might estimate that you need an additional $200,000. Under-capitalization is the number one cause of business failure, so this cash buffer is a “must-have.”

Add that buffer amount to your initial capital requirements and you’ll need $1,435,000 during the first year of operation.

To present the best, most transparent picture to investors and lenders, prepare a statement of capital needs on a month-by-month basis, showing working capital requirements and projected business income. Show them what you need, justify those needs based on solid projections, and clearly demonstrate how you’ll pay back borrowed funds.

Have you determined your capital needs? Are you looking for a solution? You may want to learn more about Working Capital Loans.